Why Bonds Are Still Essential for Diversified Portfolios

Article by James Liu, CFA. Founder and Head of Research Clearnomics.

While 2023 has been a better year for bonds after last year's bear market, rising interest rates over the past three months have acted as a headwind. The U.S. Aggregate bond index has gained 0.6% this year, down from a peak return of 4.2% in April. Similarly, corporate bond returns have receded to 1.8% from 5% prior to the banking crisis earlier this year. High yield bonds, which are volatile and often behave more like stocks, have hung onto their gains with a year-to-date return of 6.6%. At the same time, rising yields mean that bonds are able to generate more portfolio income than at any other time over the past 15 years. What do long-term investors need to know about recent swings in the bond market and how it affects their portfolios?

Several market and economic factors have created uncertainty in the bond market. First, recent events have led to swings in interest rates beginning with the U.S. debt downgrade by Fitch Ratings on August 1. This jump in rates had ripple effects across the market since U.S. Treasury securities serve as a benchmark for riskier bonds. However, just a week later, Moody's downgraded 10 banks, placed six under review, and shifted the outlooks on 11 to negative. These ratings and outlook changes briefly renewed concerns over the financial system which caused interest rates to fall. Since then, there have been concerns around the supply and demand of Treasury securities, worries over China's housing sector, and more.

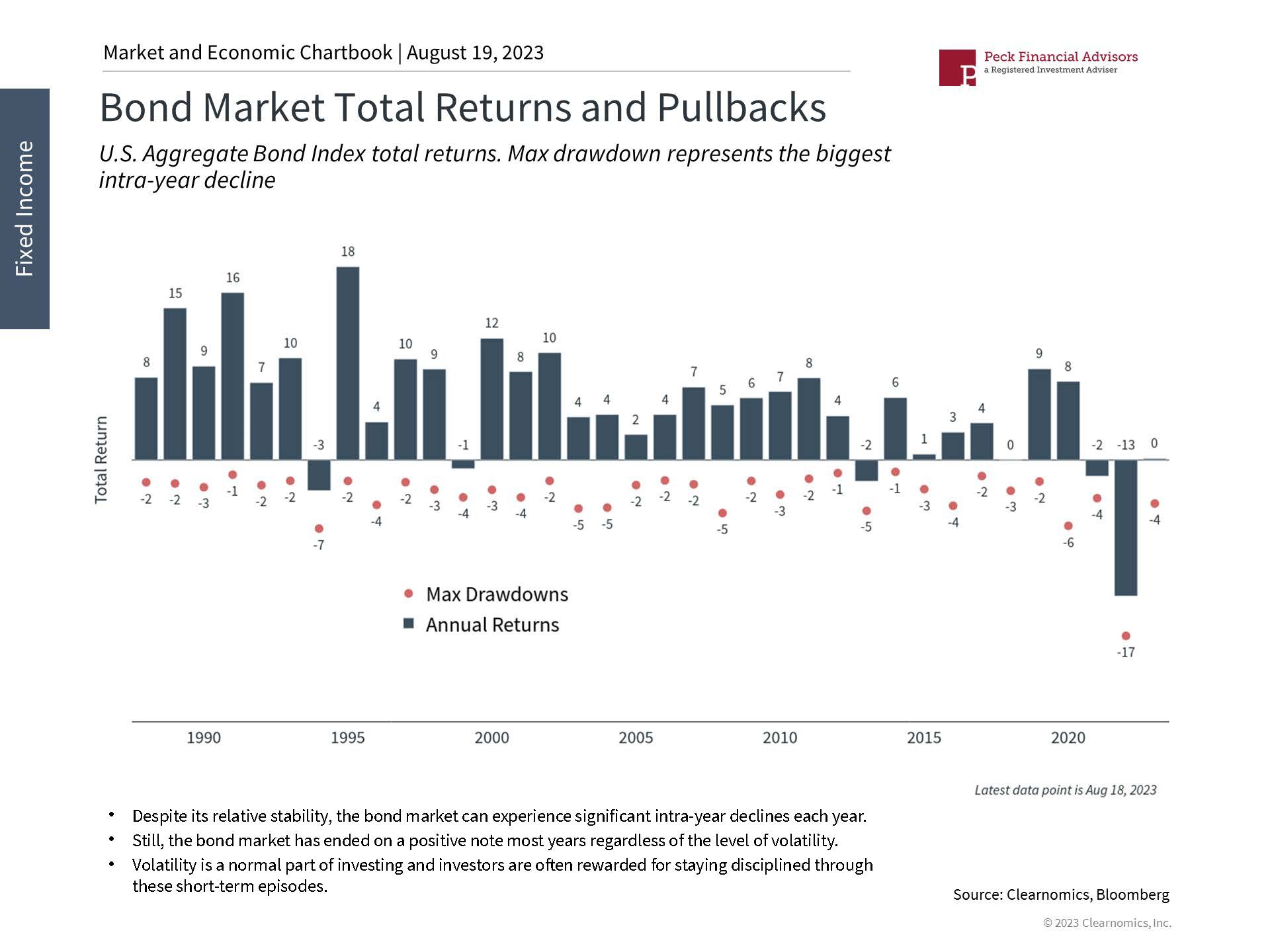

The bond market is having a better year than in 2022 despite recent volatility

All told, these events caused large intra-day rate swings with the 10-year Treasury yield rising to 4.2%, then falling to 3.9%, before surging again over the past few days. This volatility directly impacts bonds since prices and interest rates are two sides of the same coin. In general, rising interest rates lead to lower bond prices, and vice versa. One intuitive way to understand this is that the cheaper you can buy a bond with a specified payout schedule, the higher your eventual return, or yield, will be.

Despite these changes in rates and bond prices, it's important to maintain perspective on the bond market behavior of the past two years. Last year's historic surge in inflation resulted in the worst bear market for bonds in recent history, as shown on the accompanying chart. This year, bond returns have mostly been positive, and the largest intra-year decline of 4% is well in-line with historical patterns since most years experience similar declines between 2% and 5%. So, while bond prices are generally much steadier than those of stocks, history shows that fluctuating interest rates result in some bond market swings each year.

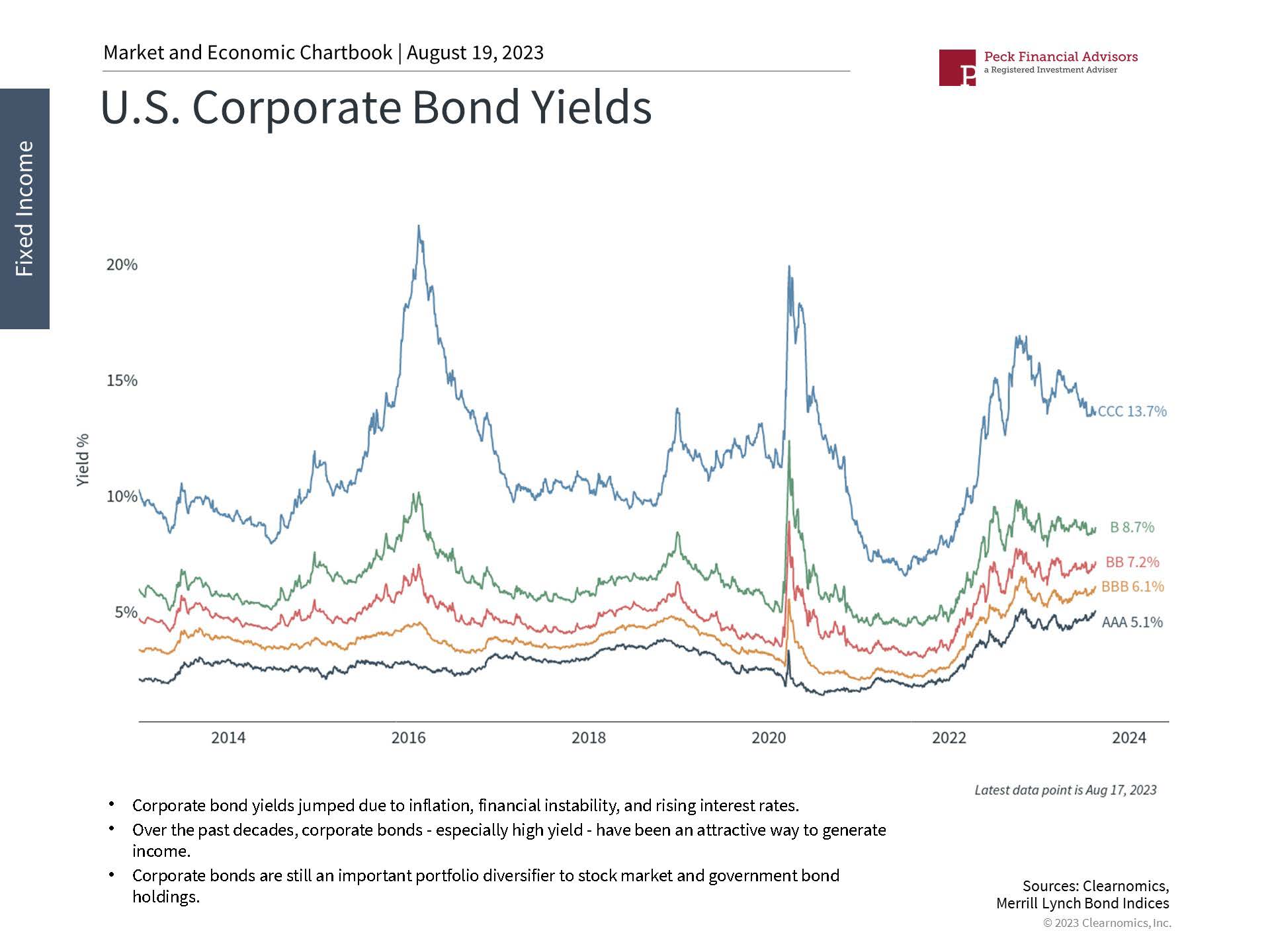

The yields on riskier bonds have fallen

Second, while the Fed is expected to keep policy rates high, there is less pressure to hike rates again as inflation improves. The latest Consumer Price Index report shows that price pressures are not only easing, but that headline inflation is already back to the Fed's 2% target when considering the latest annualized rate. Core CPI is also just under the target at 1.9% on an annualized basis and the trend is deflationary when shelter costs are also excluded. These numbers are important because they represent what is happening to consumer prices today, compared to the more commonly cited year-over-year measures that tend to be more backward-looking.

So, while the Fed has penciled in one more rate hike this year, markets believe this may not be necessary. The probability of a so-called "soft landing" has increased as economic growth has remained steady as well. This has helped to reduce credit risk concerns which were elevated during the banking crisis. As the accompanying chart shows, yields on riskier bonds have come down as recession concerns have faded and corporate earnings have beaten low expectations. Ironically, only the yields on the highest rated bonds have increased due to the U.S. debt downgrade. All in all, this means that even if a recession does occur, markets expect that it would be mild and that companies would still be well-positioned to repay their debts.

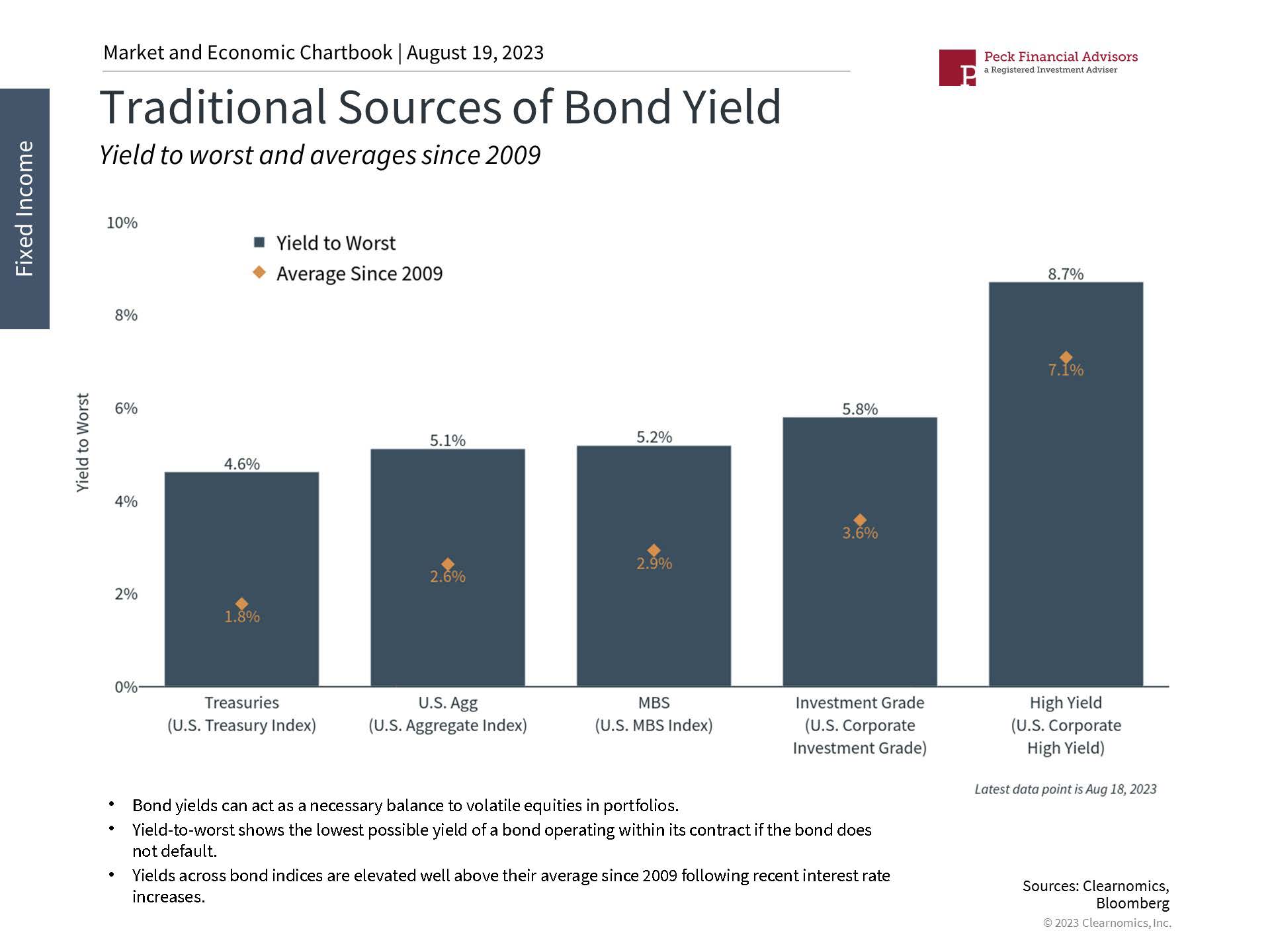

Bonds are offering attractive yields for long-term investors

Finally, investors can be better positioned to generate portfolio income today, without "reaching for yield" by taking inappropriate risks, than at any point since the global financial crisis. A diversified index of bonds now yields 5% - nearly double the 2.6% average since 2009. Investment grade corporate bonds generate 5.7% and high yield bonds 8.5%. In contrast, the forward-looking dividend yield on the S&P 500 is now only 1.9% after this year's strong rally. This is further evidence that diversifying across stocks and bonds continues to be the best way to construct well-balanced portfolios that can achieve income and growth, while withstanding different market environments.

The bottom line? The bond market continues to face challenges due to the uncertain economic environment. Still, this year's bond performance is a sharp reversal of last year's bear market, and the level of volatility has been in-line with the typical year. Most importantly, attractive yields underscore the need for bonds in long-term portfolios as inflation improves and the economy recovers.